The Irish Salon Owners Guide to Tipping Laws, Tax and Compliance

Are you prepared?

Here’s what you need to know

The Payment of Wages (Amendment) (Tips and Gratuities) Act 2022 came into effect in December 2022.

The legislation applies to ’employer-received’ tips

– i.e. tips paid by card.

According to the legislation, employers must:

Employees can complain to the WRC if you have not complied with the Act

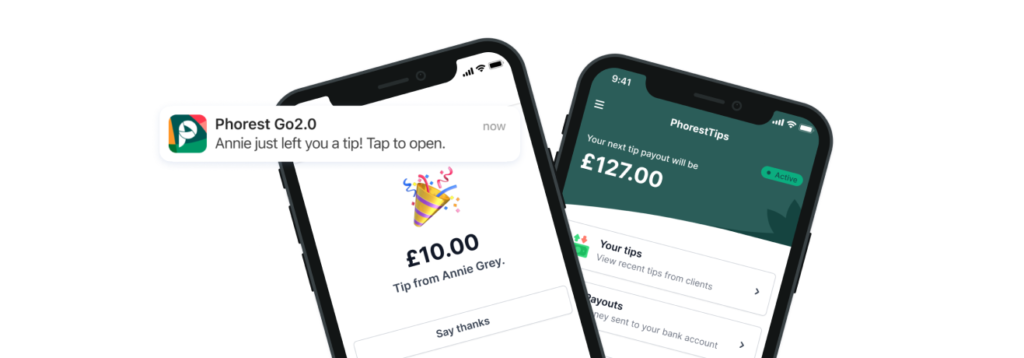

Phorest is here to support you

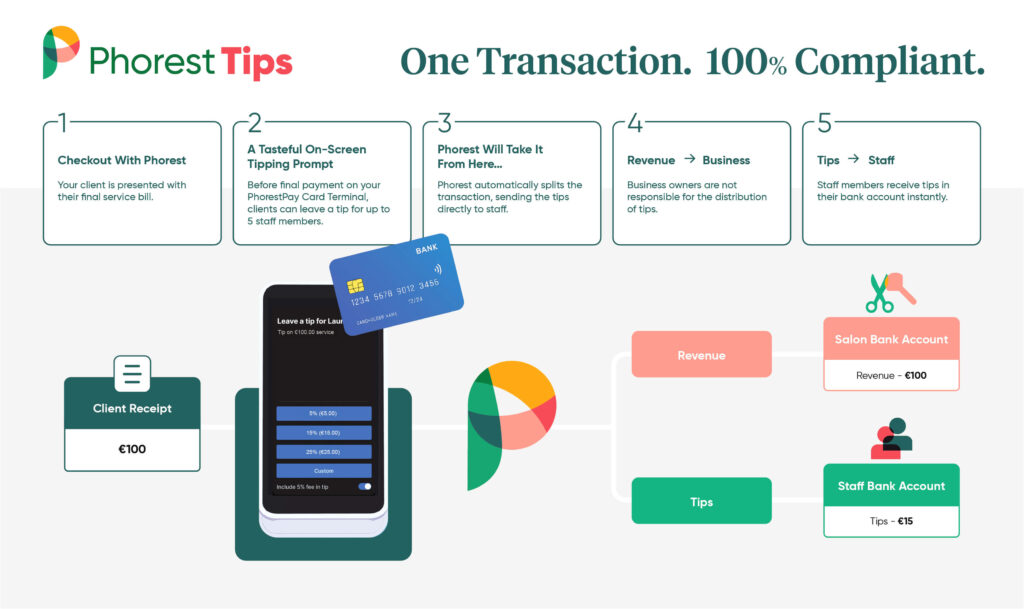

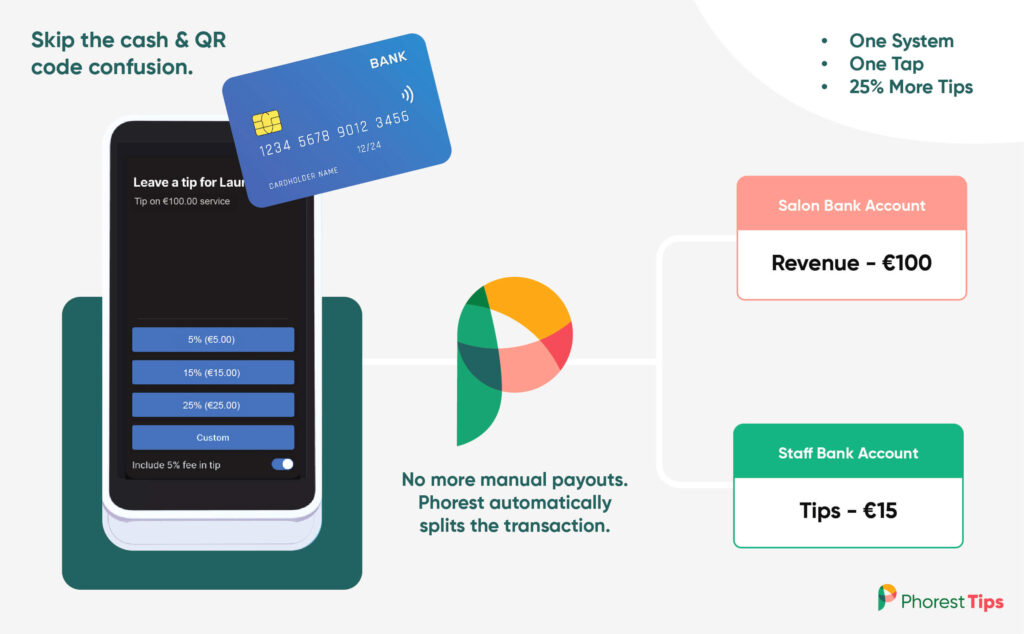

Phorest makes things easier by sending each employee their tips straight to their bank account, so they are not ‘employer-received’. Stylists and therapists get their tips into their account instantly, at no cost to the business. And there’s no QR code chaos for your customers.

A Win-Win for Clients, Business Owners & Your Team

A simple, thoughtful way for clients to show their appreciation, without the need for cash or QR codes

On average, stylists and therapists see a 25% increase in tips when using an integrated PhorestPay Card Terminal

Already with Phorest?

Get more info

Not yet with Phorest?

Book a demo

Enter total monthly tips to see how much tax and fees salon owners and staff can save with PhorestTips*

Use the slider to input the total monthly tips taken across your employee base*.

Standard card payment

Tipping app

PhorestPay card payment

Cash

Payroll

Tipping app

PhorestTips

Cash

* This example assumes the employee is a standard rate tax payer – i.e. earning below €42,000 per year

Already with Phorest?

Get more info

Not yet with Phorest?

Book a demo